EUR/usd

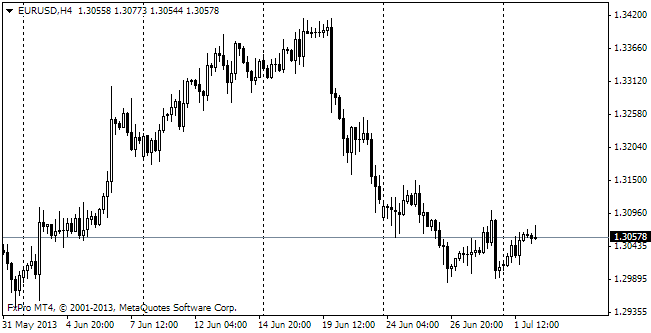

The CBs of the world's biggest economies keep moving in the opposite directions. The main currency pair received a double blow yesterday. It was somewhat unexpected as occurred neither on the publication of the Fed's meeting minutes nor the release of statistics. Advocates of the technical analysis could triumph yesterday. For 10 trading sessions the single currency had been moving inside the narrow ascending channel and, as a result, had driven the pair in the overbuy zone, so when a correction broke the support of the uptrend (1.3510), it intensified the decline. Eventually, the movement carried the pair away to 1.3413 against the intraday high of 1.3570. Now let's delve into the reasons for such aversion to the euro and interest in the dollar. A couple of the ECB's insiders made it clear that the Bank was considering introduction of the negative interest rate at 0.1%. As we wrote before November's meeting, this step will be a penalty, giving a signal for banks to issue loans instead of parking excess cash with the CB. The cut of the refinancing rate and the ECB's marginal lending rate is a ‘carrot' for the banking sector, which allows getting money at a lower interest rate. The reduction of these very rates in November reflected the soft attitude of the committee and helped EU banks due to the decrease in the differential with the lending rate. If the deposit facility rate is negative, it won't be beneficial for the banks to keep excess cash with the ECB, so they will have to choose either shift the cash to other banks or direct it into loans for households and business. Both the options are much more pernicious for the euro than the cut of the refinancing and lending rates. The second blow was provoked by the release of the October meeting minutes of the Fed. The minutes indicated readiness of the Committee to start tapering already at the coming meetings. It somewhat surprised the markets, which had decided on October 30 that the Fed on the contrary postponed this moments for an indefinite period. The picture is getting clearer – the US CB needed data on the economic performance in October to see how negative the government shutdown was. As seen from yesterday's retail sales statistics, it didn't prevent them from growing by 0.4% instead of the expected 0.1%. With the Fed taking such a position, the strong US statistics again increase a chance of tapering in December or at the end of January.

GBP/USD

Once again the pound suffered not for itself. The BOE's minutes didn't produce any particular effect on gbpusd, but for all that we see some growth against the euro, which is quite understandable. The main idea of the minutes is that unemployment when it reaches 7% won't cause an automatic rate increase, but only give the Committee a signal to reconsider the nature of the recovery. Anyway, rumours about the ECB's rate and sudden severity of the Fed helped the pair break its series of ascents, indicating a possible reversal at 1.6170. Now the pair is almost a figure lower – at 1.6080.

USD/JPY

The dollar's growth didn't allow the yen to perform full-scale correction. The pair is now at 100.30 and a bit earlier rose to 100.50. The latter level used to be a good resistance in September and July, but now we don't see any serious reasons to worry about the fate of the uptrend. We're looking for the right moment to start purchasing.

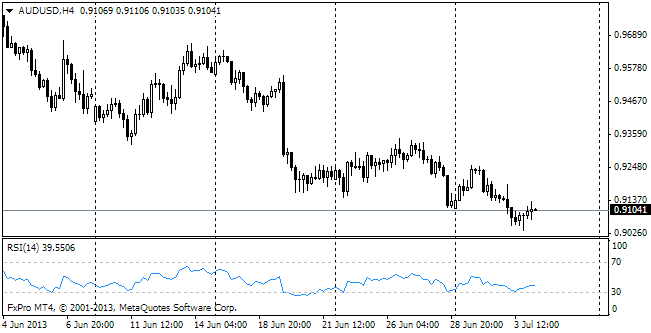

AUD/USD

The Australian dollar felt bad even without the US news and with it even worse. The desperate attempts of bulls to consolidate above 0.9400 were ruined yesterday. Now the aussie is trading below 0.9300. Very close there is a support at 0.9280, breaking of which may turn into the total surrender of Aussie-bulls. If you'd like to stake on AUD, consider audnzd for now.