EUR/usd

The US stock market feels more and more confident at a new level. S&P 500 has exceeded 2000 and the global asset market reached the capitalization of 66trln, as calculated by Bloomberg. Before the global financial crisis appreciation of the stock markets often turned out to be USD's decline and strengthening of the currencies in the developing countries, which also affected EUR and the pound. Though the pound in theory can follow this very tendency against growing chances of the rate increase earlier than in the USA (see below), the euro's recent weakness has been quite reasonable. And don't say that we haven't mentioned it before. Before 2008 growth of stock exchanges had been fed by mildness of the US monetary policy. Though the rates had been quite high, the macroeconomic situation had required a sharper increase of the rates and their higher level after the crisis of dot-coms. Thus, the dollar and mainly the yen had served as funding currencies. Now there are plenty of funding currencies, including the euro and the pound. However, now investors have to watch which of the biggest state borrowers will be the first to leave this band. It is not hard to make out that Britain will be the first, the USA will be the second, Australia and Canada will probably follow next and the eurozone will go after them. Japan with its chronically low interest rates, apparently, will bring up the rear. In this connection demand for the euro may lead only to success of the EU economy, which will make investors reconsider the prospects of the regional monetary policy. During the financial crisis the US statistics were treated as a leading indicator of probable events in Europe and the developing countries. But now it is already a different story. Each follows its own way. The crisis is one for all, but then each country recovers at its own pace and by its own means. In other words, the strong US data will support the dollar and the markets rather than contribute to raising the global optimism.

GBP/USD

Yesterday the cable was pushed down to the local lows, making it test the support at 1.6530 again. The bulls manage to retain the defensive at that level for now and this morning even tried to counterattack and raised gbpusd to 1.6570. At the end of the month we will see how successful it is. In our opinion, traders raised the British currency too high over the previous year on drawing near the forecasted date of the policy toughening, and now we see just the opposite, market players are persistently getting rid of the cable. It is obvious from the poor performance of EURGBP. In our opinion, the sterling will be out of buying interest until there is a clear signal of the rate increase or better until the very increase. But now it would be more reasonable to sell the pound or look for a suitable moment to buy. Probably, the stake for the pair's decline will not be justified: risks of the impulsive upsurge are too high.

USD/JPY

Yesterday bulls made an effort and raised the pair up to the daily open after the drop at its beginning. It is the best they could do. In the short term, despite strengthening of the stock indices bears will be still in the lead. The end of the month, in our opinion, may well go under the banner of correction of USD's preceding growth, though in the long term there is hardly any threat to the dollar's rally.

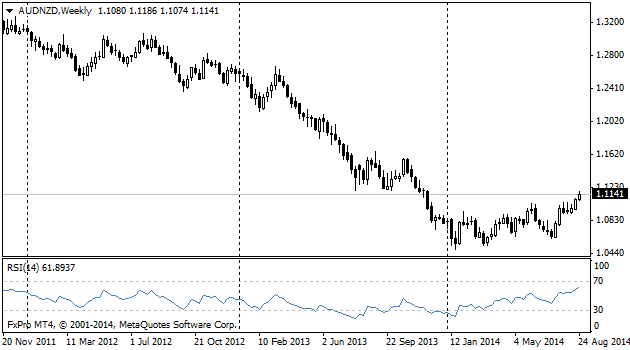

AUD/NZD

Despite the constant toughening of the RBNZ's monetary policy and the RBA's unceasing pressure on its domestic currency, the aussie coupled with the Kiwi has contrived to offset its losses. Yesterday the pair rose to 1.1180, which hasn't been seen since last December. Forex is getting ahead of itself and, as a result, is making up for the promised pause in the RBNZ's rate increases and absence of any action on the part of the RBA. In our opinion, this trend with some breaks will hold for the next few months.