EUR/usd

The single currency didn't manage to recover yesterday. eurusd was below 1.32 almost all day long yesterday, though the major rivals of the single currency felt much better. Besides, S&P 500 crossed the level of 2000, which was a significant moment for the markets. The index didn't move far from this level and went on the defensive right after hitting the level. As we mentioned yesterday, the initial weakness of the euro was maintained by the divergence between the US and EU monetary policies, once again emphasized by the comments of the Fed's and ECB's governors in Jackson Hole. But further there were new reasons to sell the euro against the dollar and others, for example, against the pound. Ifo's index of business climate in Germany fell short of expectations. So we get a picture where Germany's business climate, according to ZEW and Ifo, reflects the obvious deterioration and vigilance. Yet, the PMI rates are still a bright spot here. They still speak about expansion of the economy. The Services PMI, for instance, slightly declined in August in comparison with the preceding month, but still remains at the highest level since 2011. This state of affairs indicates steadiness of growth inside the country as services are generally offered to Germans. But in the meantime, the production sphere – the driver of economic and employment growth – is slowing down and the corresponding index is now at the lowest level since last October. Probably, it is connected not only with the sanctions against Russia and its retaliatory sanctions, but also with the attempts of the peripheral countries to become more competitive and rebalance in search of growth drivers outside the country, rather than inside it. Don't you think that the eurozone, so self-sufficient before, is too persistent in seeking growth drivers outside? China is following the same way and America also has such intentions.

GBP/USD

The British pound was in demand yesterday afternoon due to weakness of the euro, but at the end of the day it still fell under selling pressure. The pair is generally trying to find support at 1.65. So, today closer to the end of the Asian session gbpusd pushed off 1.6560 and closely approached 1.66. BBA Mortgage Approvals are published today. Analysts expect growth after the downfall in April and May. Our opinion has been formed with a glance to the price behaviour in the housing market, which demonstrates obvious decrease in demand and prices, so we are waiting for this publication with caution. The overwhelming majority of mortgage approvals in Britain are issued at the floating interest rate. And the expectations of its growth may deter buyers. Besides, the ratio of housing prices to earnings has again reached the pre-crisis levels, i.e. became unsteadily high. We shouldn't be surprised if the British will show more caution in buying new houses in view of earnings stagnation.

USD/JPY

Despite the highs of the stock market, with the Japanese yen traders are more cautious. usdjpy suffered slight profit-taking yesterday and today after the impressive growth. There is a feeling that bears haven't eased their grip and are simply waiting for a suitable moment to reverse the trading course and channel it back to the trading range, where the pair resided for the preceding 6 months.

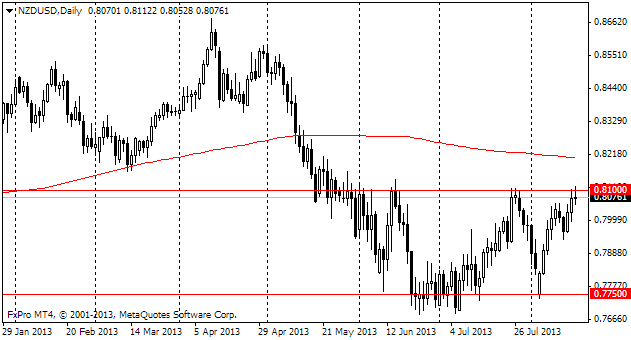

NZD/USD

The New Zealand Kiwi got a blow from the poor foreign trade statistics today. In July the deficit made 692bln against the expected 475bln and the surplus of 242bln a month before. The main problem is export reduction from 4.18bln to 3.7bln with significant growth of imports from 3.94 to 4.39. Of course, these data can get more volatile month after month, but now we see a growing fear that the period of high exports in New Zealand will change for a period of more measured rates.