EUR/usd

Monday didn't abound in important news releases and statistics. Anyway, the single currency managed to slightly grow against the dollar and the pound. At the very beginning of trading in Europe EURUSD rose by 40 pips due to the stronger risk demand, which we highlighted in our yesterday's review. However, by the end of the day the positive had dispersed. To some extent it was a result of draghi's claims in the EU Parliament that purchases of public and private debt fall ‘squarely' within the ECB's mandate. Many officials in Germany and other core countries, including members of the ECB, are constantly opposing such claims, but investors attach more importance to the words of the central-bank president than to other comments. At least, having realized that the ECB can ease the policy even despite some resistance of Germany and the like. Today traders' attention will be riveted on a speech. This time on the coming speech of Janet yellen before the Congress. Yellen is expected to shed more light on the plan of tapering and policy toughening. Analysts suppose that she will talk about possible economic acceleration in the second quarter after the dreadful rates in the first one. Besides, today we will get data on the US retail sales, where we also can find confirmation of the strong forecasts for the second quarter. Anyway, traders don't hurry to purchase the US currency, fearing that Yellen will be too cautious and retails sales will turn out to be poor. As far as technical analysis is concerned, the ascending support really deserves attention. This line is passing through 1.36. However, in case of strong sales data and Yellen's confidence about strength of the economy, breaking through this level is able to intensify selling of EURUSD.

GBP/USD

Yesterday the sterling suffered profit taking. Without any important news the cable tumbled below 1.71. Probably, it was caused by the release of data on speculative long positions on the British currency. Last week's data indicated reduction of stakes for growth in GBP on the side of hedge funds and other big speculators. Their behaviour is quite reasonable as the sterling has been rallying for about a year, so the profit potential is quite exhausted. Besides, last week's British statistics were either neutral or negative. So it is good time to lock in profits. This week there are a lot of significant data scheduled for release this week, including CPI and employment as investors can still reevaluate their views in this or that direction.

USD/JPY

The Bank of Japan expectedly sticks to the policy of extending the money base by ¥60-70trln yearly and forecasts reaching 2% of inflation in the medium term. While the members of the Bank's governing board adhere to their earlier forecasts and programmes, investors and analysts are reducing their stakes on further easing by the BOJ. The inflation sentiment now is also supported by increase in prices of energy, which Japan is actively buying from the outside after the decrease in atomic energy production.

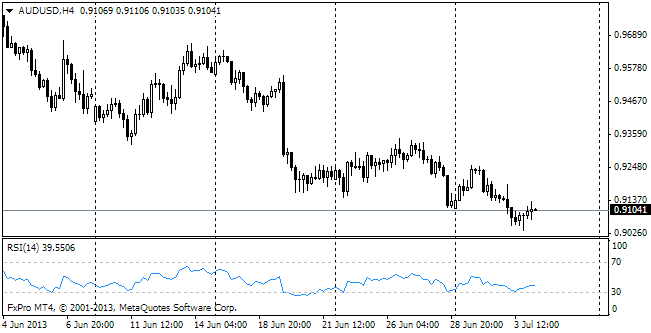

AUD/USD

The aussie got modest support on the release of the RBA's meeting minutes in July. They say that the current low interest rates can boost the demand. In general the bank was disposed to maintain the interest rates at the current level for a while. The neutral approach to the rates is customary for traders, following the RBA in the recent months, but last week the Aussie received a blow as Reserve Bank Governor Stevens in his speech surprisingly didn't exclude a possibility of policy easing. Upon the whole the Aussie is hovering around 0.94 already for about a week.