EUR/usd

The market showed a strange reaction to Putin's speech yesterday. Market participants took positively that Russia didn't lay claims on the rest of pro-Russian territories of the Ukraine and other post-Socialist countries. Stock markets unanimously set out in the upward direction, whereas the reaction of currencies was contradictory. The initial growth of the euro to 1.3940 (due to risk demand) was followed by a pullback and new intraday lows at 1.3880. If we exclude nervousness caused by the news, the pair has been staying at the same level since the beginning of the week. The focus of attention is expectedly shifting from Russia and the Ukraine to the Fed's decisions. In our opinion the geopolitical tension still exists. We need to wait for the second round of sanctions. The news that NATO isn't threatening to send troops was already taken as good news by the markets. Generally speaking, Europe, seeing such a resolute position of Russia, may hurry up with including of the Ukraine into the EU, even despite the fact that earlier no one could expect such vim from Europe, seeing how many rounds of negotiations the bailout of Greece took. But let's divert our attention from Europe. Today the markets will be focused on the Fed's press-conference. Yesterday we highlighted the importance of this event due to an opportunity to hear details on the future policy of the fomc. We hope to hear hints at acceleration of tapering in the coming months if the economic situation doesn't get much worse. Only resoluteness can help the dollar. Otherwise, the US currency may continue to drift down against the euro.

GBP/USD

Yesterday the British pound was actively depreciating against the dollar, which was quite unusual with the impressive performance of stock exchanges (lately we've seen quite a strong positive correlation between them). The pound got in demand only towards the end of the Asian session. Today's employment statistics were of the highest importance – it indicated decrease in unemployment claims by 34.6K. This indicator has been falling impressively since the previous year. But the sterling failed to benefit from those favourable data as before that it had partly exhausted the demand and will have to deal with the budget plan for the current year yet. Thus, today the sterling will attract attention of traders, searching for active instruments.

USD/JPY

For 19 months in a row Japan has been facing trade deficit. In anticipation of tax increase in April economists hoped for stronger economic data than we've seen lately. Altogether it creates a sad picture for the world's third economy. In our opinion, it increases a chance of more active stimulation by the BOJ. But now it is too early to speak about that as the next meeting is held only in the middle of the next month. In the meantime, usdjpy remains pressed against 101.50.

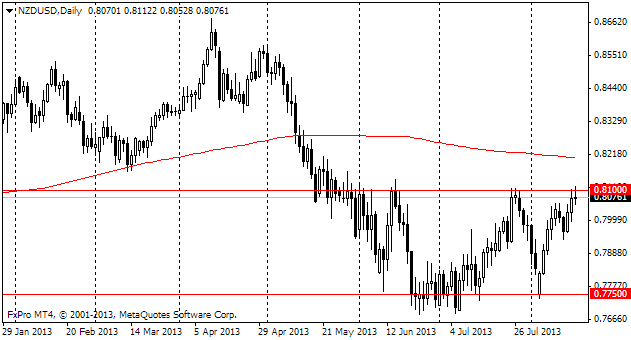

NZD/USD

The Kiwi keeps growing. The New Zealand dollar is trading at quite unsteady levels above 0.8600. It was here for less than two days a bit over a year ago. Now the main risk is posed by the release of GDP statistics this night. It is expected to grow by 1% and the annual growth rate is forecasted to slow down to 3.1%. The Kiwi remains overbought as has been written earlier, but for selling to start we need confirmation of the reversal. Without it the growth may continue for a few more days.