EUR/usd

Yesterday the single currency fell under pressure after Reuters' message that the ECB could start purchasing corporate bonds already in December. That news deprived the euro of about 0.7% and pushed eurusd down to 1.2700. Formally this level held out , but it seems to be just a question of few days, when the single currency will continue its downward movement. Investment banks have already hastened to announce the end of the correction and the beginning of a new downward trend with the targets at 1.25 and in the longer term at 1.20. Weidmann, Bundesbank President and the main oppositionist of the ECB's current policy of easing, said last week that bond purchases are a shift towards a quantitative easing philosophy. Well, it was obvious already in September that the ECB would try to decrease interest rates by extending its balance sheet with various assets. Besides, the fundamental indicators like inflation, business sentiment and unemployment are very far from the levels, when the mild policy of the CB can do harm. But this way or another, the ECB's course towards easing forces the single currency to depreciate and supports the markets. Probably, we need to get used to the fact that the euro will be a funding currency for the coming years, ousting the dollar from this place. So, don't be surprised at inverse correlation between the euro and stock exchanges. As you remember, before the crisis this dependence was direct. But yesterday the market was affected not only by the news on the euro. Market participants were attracted by the report on the US existing home sales. The seasonally adjusted indicator of home sales has reached the highest level for 12 months with the rate of annual sales at 5.17bln. It makes growth by 2.4% against the previous month and by 12.6% against the local high in March. The amount of unsold homes has also declined from 5.5M to 5.3M. However the prices slightly fell from June's high of 222k to 209.7k in September.

GBP/USD

Yesterday the British pound was falling under the general pressure, which stock indices were also suffering for the most part of the day. However, it missed their upsurge – the highest intraday growth of S&P 500 over the last year. As a result, the pair faced an unconquerable resistance at 1.6200 and at the end of the day it was pushed down by almost a figure. Today the pound is at risk of falling, should the fomc's meeting minutes prove to be milder than in the previous months. Yet, the movement shouldn't be very strong since it has already built into the rates.

USD/JPY

The growth of stock indices has put quite a moderate impact on the yen. It has returned a part of its gains since the beginning of the week, but still remains below 107.00. The trade balance again doesn't look very encouraging. Though exports and imports exceed expectations, which speaks about stronger business activity, the overall balance still leaves Japan a pure importer, which is not typical of it. This situation will probably continue putting pressure on the yen. Till the end of the year the dollar is quite able to reach ¥110.

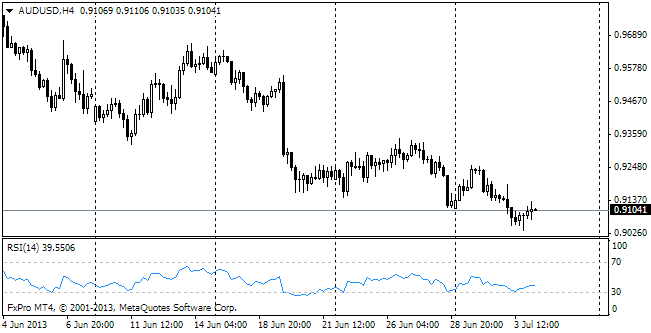

AUD/USD

The aussie is abstaining from sharp movements despite the relatively bullish inflation data. The major index of consumer prices grew by 0.5% in 3Q (against the expected +0.4%). The annual price growth remains within the target channel of the RBA (between 2-3%%) at 2.3%. Yet, against the previous quarterly rate of 3.0% it is a slowdown. The index of leading indicators keeps decreasing, which also arouses pessimism. This index lags behind the trend rates of growth by 1.16% and this divergence has been getting more and more dramatic since May.