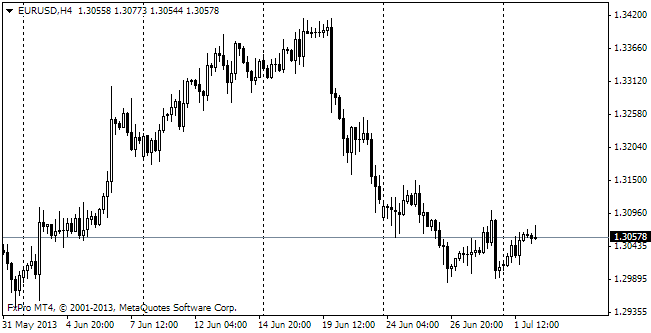

EUR/usd

The single currency couldn't stay below 1.3400 for long. Bulls came to their senses and under the cover of the favourable EU statistics were purchasing the euro. The poor rate of France's Manufacturing PMI (47.8 against the expected 49.6) was pushed into the background by Germany's manufacturing stats, which proved to be better than forecasted (52.5 against the expected 52.3). The services sectors of these countries also performed below and beyond expectations accordingly. The flash index for the entire eurozone hit the level of 51.5 in November, which is slightly better than the October rate of 51.3 and slightly worse than the forecasted 51.6. The EU Flash PMI Composite, in the meantime, fell from 51.9 to 51.5, confirming the tendency for growth slowdown after the upsurge in August-September. Coincidentally, the business activity was slowing down along with the rise of the single currency. We still consider that in the coming months these stats will become even worse because of the euro's appreciation in this period. As a result, it may contribute to weakening of the single currency in no small part due to speculations about possible introduction of the negative deposit rate against the cut of the base interest rate. By the way, yesterday Draghi spoke in detail about this. After yesterday's news he came under pressure of journalists. Answering their questions, he pointed out that there was nothing new about that discussion as the ECB was considering various ways, but that measure got lots of negative comments among the members of the governing council. And we know who they are, remembering keen criticism regarding the rate cut from Germany's representatives. And already after Draghi's words the pair came under influence of the US statistics. The number of unemployment claims is decreasing – yesterday it hit 323K, thus making up for October's rise. The number of continuing claims has been fluctuating since August and remains below 3bln. The US labour market is doing quite well, which supports the markets. Yesterday Dow closed above 16000. It should attract attention of market participants and also boost growth. S&P 500 also offset the losses it had suffered during the small correction in the preceding days. Despite the Fed's meeting minutes, neither stock markets nor Forex believe that the bond-buying progamme will be terminated soon. Anyhow, the meeting minutes date back to October 30, while Bernanke and yellen spoke at the beginning of this week and could refer to more recent data.

GBP/USD

Yesterday we said that the pound suffered not for itself and if even the euro recovered, the sterling felt even better. With growing markets in the background, it managed to get close to 1.62. And if today we see further growth of stock exchanges, the pound may return to 1.6250, which the pair couldn't break through in the first and the last decades of October. The double top still hasn't ended in a reversal.

USD/JPY

The yen is being sold. This process began a bit later than expected (earlier it was spoken about the middle of October), but yet it began. usdjpy yesterday broke through 101. As expected, the level of 100.50 (the preceding local high) didn't become a serious resistance. The next target – 101.50 – is within the walking distance now. The only obstacle to it, in our opinion, can be seen in Friday's profit taking.

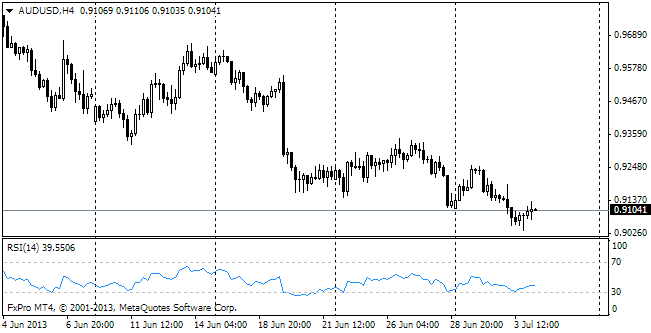

AUD/USD

Glenn Stevens puts unstoppable pressure on the currency entrusted to him. Yesterday the aussie received a blow on his comment that the RBA was ‘open-minded to currency intervention'. Yet, its effectiveness is under question, as was also mentioned. The Australian currency was called overrated not only by the RBA, but also by the IMF. The Aussie is having a hard time.