EUR/usd

Despite the tangible pressure, which had weighed upon the single currency in the first half of the day, the US session again was marked by purchases of the euro and in the US stock markets. By the end of the day stock indices had entered the positive territory and by now futures have already recouped two thirds of the correction, which have been in place since the end of the previous week. EURUSD got above 1.39 during the New-York session yesterday and has been steadily trading above this level since then. It was caused by comments of Germany's Finance Minister Schäuble. He characterized the current interest rates as very low for the medium term. Besides, in his speech he mentioned a possible resolution on the Ukraine and also reminded of the strong fiscal position of Germany. In other words, we shouldn't expect that Germany will lift its pressure off the ECB and turn a blind eye to softness of the monetary policy. But for deflation in the troubled EU countries, Germans would advocate the rate increase already now. It should be also noted that the price index under consideration (0.8% y/y) is harmonized, which means tax-adjusted. Actually, tax increase in the countries seeking fiscal consolidation, conceals deeper decline of prices for goods and services. It is favourable as far as competitiveness of exports is concerned, but it also reflects poor demand and lower living standards. Moreover, the euro, which has appreciated by 10% against the dollar over the last year, simply ruins all the competitive advantage from decrease in prices and salaries in the southern EU countries. In our opinion, the euro has little chance to stay at the current or higher levels for long and soon will go into the lingering trend down to 1.30.

GBP/USD

The British pound went through short-term selling yesterday. At some point it fell to 1.6567, but found a support at that level, not least of all because of the across-the-board selling of USD. As a result, we see an obvious correlation between stock exchanges and gbpusd, though the latter is now lagging behind the markets. As has been mentioned earlier, there is a feeling that the British economic growth has already passed its peak, and officials mainly say that they are not going to hurry with increasing the rates. Britain's NIESR ( a very reputable institute) is of a more cautious opinion about tightening of the policy, expecting the first rate increase only in the second quarter of 2015.

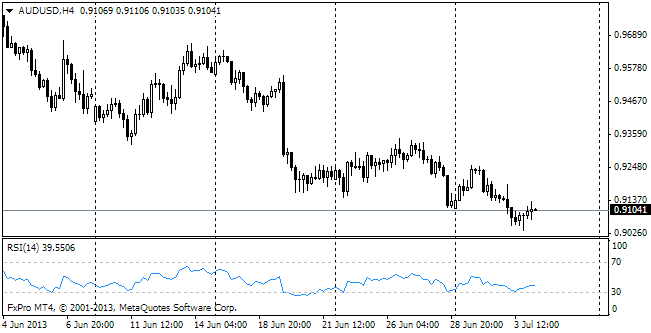

AUD/USD

The Australian labour market surprised with significant employment growth. The full-time employment rose by 80.5 in February. For comparison, in the USA where population is 14 times as high as in Australia, the February employment rate was only twice as much. As a result, the excellent employment statistics and yesterday's weakness of the US dollar helped the aussie grow from 0.8930 to 0.9080 for less than a day. The country's statistics are more neutral now, so we expect a few months of AUD's consolidation in the range of two-three figures around 0.9000.

NZD/USD

The increase in the major interest rate, albeit surprising, nevertheless aroused stronger demand for the Kiwi. Apparently, before the decision there had been some people, treating that issue with caution (we among them). Export prices contribute to the strong demand for the Kiwi, but the latter is now very close to its historic highs. It was higher only for a little while in 2011 and 2013. The depreciation of audnzd since the beginning of 2013 is also very remarkable. This pair is close to its historic extremums too. Earlier it always found strong support below 1.05.