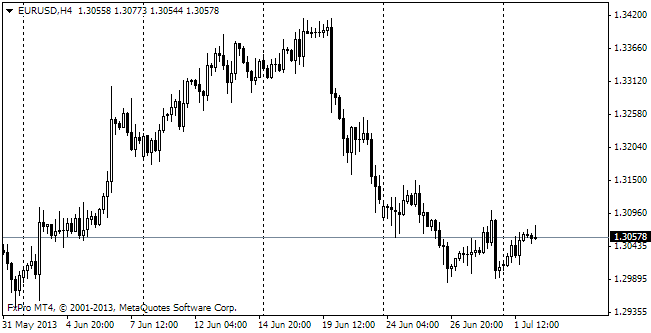

EUR/usd

eurusd remains in the uptrend. But yesterday it seemed that we turned on a serious resistance at 1.35. Thus, on the one hand, we've got a series of ascending intraday lows, but on the other hand bears are putting up strong resistance at 1.35. By the end of the week the market has stuck somewhere in between 1.3418 and 1.3490, which were hit during the European and US sessions (now it is 1.3450). It's remarkable that for all that stock exchanges don't feel any confusion. For them the situation is pretty clear. The next chairman of the Fed, Janet yellen, is going to pursue the same policy and seems to be quite loyal as far as the stimulus tampering is concerned. Along with the strong employment and housing statistics in October, we've got a combination of the accelerating economy and soft stance of the CB. Under different circumstances it would be pernicious for the dollar, but now Forex has to balance between the soft stand of the Fed and the ECB. The committees of these two CBs have both advocates of a softer position and members who have being speaking about risks of this approach. Today we do not expect any serious shifts as there will be little economic statistics released. Probably, only the US Industrial Production is worth considering. Yesterday's GDP statistics for the EU countries arouses quite conflicting emotions. Actually, troubled Spain, Italy and Portugal performed here better than expected. But the GDP rate in France and the eurozone in general proved to be weak. The economic growth in the region made 0.1% quarterly. Yet, the decrease against the previous year is still in place, now totaling 0.4%. The EU economy is now slightly below the rates of 2011, so we believe that hawkish views cannot be very strong in Europe. We don't expect much from this day – probably just a slight downward correction within Friday's profit-taking.

GBP/USD

Retail sales proved to be weak, but who cares? Yesterday's statistics showed that sales shrank by 0.7% in October. The annual growth rate slowed down to just 1.8%. But this news should be considered taken in the context. And the context is now such that Britain is expected to raise the rates earlier due to the strong economic statistics. This supports the British currency, which feels more and more confident above 1.60. Now trading is held at 1.6080 and yesterday the currency event tried to test 1.61 on the release of the US news. Softness of the Fed's policy prevented the decline, which had been promised by the double top.

USD/JPY

The Japanese currency seems to meet our expectations. Its weakness keeps manifesting itself and yesterday spilt over into growth above ¥100 per dollar. It was largely due to the positive performance of stock exchanges. At least here we still can observe correlation with the stock market. The level of 100 is a good psychological mark, but yet the market is unlikely to stall near it. It is quite possible that the preceding highs will be attracting bulls. The nearest one is 100.0, then goes 101.50 and farther the multiyear high at 103.70.

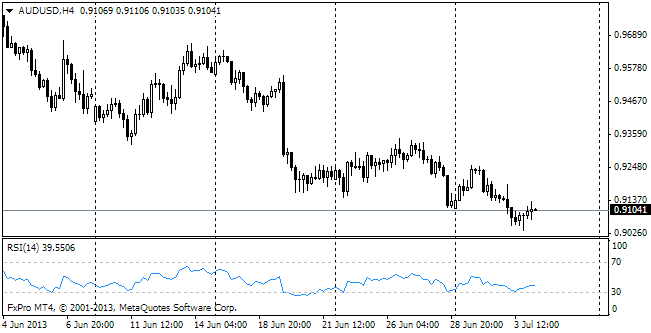

AUD/USD

The Aussie is one of the currencies, which failed to take advantage of Yellen's soft stance regarding tapering. Yesterday the Australian dollar was pushed down below 0.93. By now audusd managed to go above this mark, but it is going on quite hesitatingly.