EUR/usd

The federal reserve finally put an end to bond purchasing, as had been mentioned in the earlier plans of the Committee. It was feared that the Fed would soften its stance in view of the inflation which proved to be weaker than expected and of the recent sharp decline of the stock markets. Instead of this the Committee focused on the favourable data on employment and also on consumer and business spending, explaining that these trends can become a reason for inflation acceleration. Logic is simple here. Lower unemployment increases competition between employers, which results into acceleration of earnings growth and eventually affects spending and prices. To avoid superfluous acceleration of inflation the Fed should pursue a preemptive tactic, suppressing inflation expectations in time. The CB's concentration on the inflation stats and quite optimistic economic and employment expectations became a surprise for the market, which as a result aroused increased demand for the dollar. Since last evening the US currency has grown by a figure and a half against the euro, falling to 1.2620. But it's worthy to mention that probably it is not the end. As investors will consider the deviation between where the Fed and the ECB are heading for, the pressure on the single currency may get stronger. The short-term support line, which we spoke about for the last 2 days, was easily broken. Now attention of short-term traders is focused on 1.2600, which served as a good support on October 23 and 10. Probably, only Germany's employment statistics can help the single currency. But it should be realized that employment weakness can become another reason for weakness of the single currency. In this case the pair should be expected already near 1.2500, the lowest rate since the beginning of October, earlier reported in September 2012.

GBP/USD

With similar fierceness the dollar-bulls finished with the support of the short-term uptrend in GBP. The pair's decline below 1.61 during the initial reaction to the US news eventually provoked dramatic intensification of selling. By the end of yesterday's trading session the cable lost a figure against the dollar and has gone below 1.5970 for a while today. The nearest support is at 1.5940 and a stronger level is at quite a distance – at 1.5870.

USD/JPY

The yen easily broke through 108 yesterday. Now trading is held at 109 and it is already a serious claim for a movement to the multi-year highs at 110. Yet, it will require more reasons. It is unlikely that the market will venture an attack without any important news on the US employment or some clear comments from Japan. However, the crawling uptrend can go on due to growth of the stock markets, if any. The Fed's hawkish tone can keep influencing the stock exchanges for a long time.

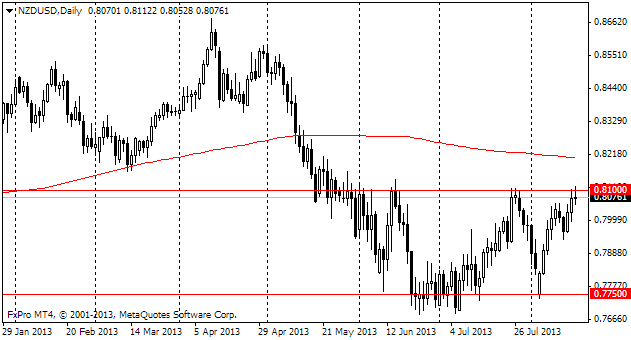

NZD/USD

The New Zealand dollar dropped not only because of the hawkish mood of the Fed, but also because of the sudden change in the tone of the RBNZ's commentary. Earlier this year the Bank mentioned that soon there could arise a need for tightening of the monetary policy. Yesterday this phrase didn't appear in the comments to the rate decision. The rate itself was preserved at 3.5% as expected. The Kiwi fell down to 0.7760, the lowest level since October 6. The nearest highs are at 0.77 and farther there is a gulf right to 0.75.