EUR/usd

The European session began with the fresh pressure on the single currency. Before the release of Final Manufacturing PMI the euro had been pushed from 1.3640 down to 1.3590. Most likely, it had been connected with the earlier reaction of the market to the inflation statistics in the German lands, which at the end of the day was to form into the overall picture. Then it turned out that the actual data failed to meet the forecasts, so the euro's decline was accounted for by fundamental factors. The EU Services PMI in May was revised down to 52.2 instead of the initial 52.5. The German index was reduced from 52.9 to 52.3. May's rate for Italy (it is never preceded by the preliminary estimate) also proved to be worse – instead of the expected growth from 54.0 to 54.3 we saw a drop to 53.2. The French and Spanish rates brightened up the negative sentiment a bit, but didn't produce much impact on the general picture. The German inflation, upon the whole, contributed to weakness of the euro. Instead of growing by 0.1% in May, the prices fell down by the same rate. In this connection the annual inflation rate proved to be at 0.9% against 1.3% a month ago. It is the lowest rate in almost 4 years. It leaves space for maneuver by the ECB and considerably increases the chances that today's data for the whole eurozone will also be lower than the expected 0.9% (economists spoke about it already on holidays). Today these data may prove to be very significant for the single currency, but it also may turn out that the market has already built the values from 0.8% to 0.9% into the rates. The most important event for the single currency this week is Thursday's meeting and market participants will hardly venture to shift the pair to another level until then. Even employment data may fail to put much influence here. Only new detailed comments by the ECB's officials may become an exception.

GBP/USD

According to yesterday's Manufacturing PMI, Britain is getting cooler, just like the eurozone. Although it is slowing down from a higher level. The rate dropped from 57.3 to 57.0 against the expected reduction to 57.1. Besides, the number of the approved mortgage loans has been decreasing for three months in a row. Yet, again from quite high rates. The sterling closed the day with a decrease, though a minimal one. Trading is now held at 1.6750 and the week opened close to 1.6765. The Services PMI release on Wednesday may become the most important news for the pound this week.

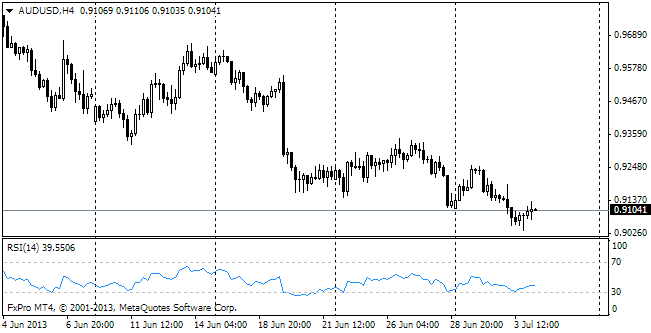

AUD/USD

The RBA kept the major rate unchanged at the lowest level on record (2.5%). That decision completely coincided with the expectations. The pair is in demand, despite the growing optimism in the comments of the RBA's governor. Stevens stopped referring to weakness of the labour market and pointed out the signs of improvement in investors' sentiment outside the extractive economic industries. The aussie returned to 0.9270 after yesterday's selling, which led it to 0.9270.

USD/JPY

Today the members of the Japanese CB spoke to the Parliament. Their comments produced a soothing effect on the markets. The officials warned about the damage, which can be caused by the too early tapering. Of course, it is bad that they don't talk about a new portion, but in comparison with toughening, so much favoured by most other CBs (except the ECB), this position looks more than peaceable and capable to put pressure on the Japanese yen.