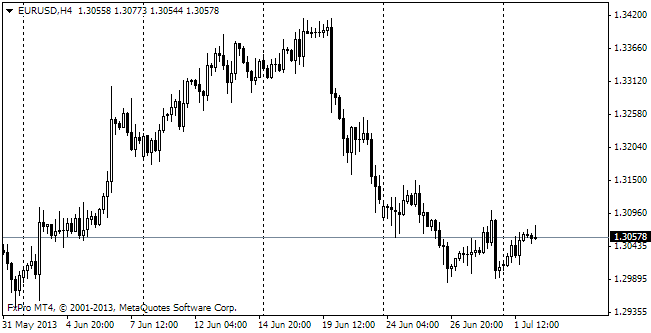

EUR/usd

The single currency came under pressure yesterday evening on the words of Jörg Asmussen that the ECB's intention to “keep the rates at or below the current levels for an extended period of time” goes beyond a 12-month horizon. Officially the CB has announced that these words shouldn't be treated as precise directions. However, we, like the majority of market players, have become firm in our suppositions. For example, when the Fed started to use the same phrase, the period of time to keep the rates low went beyond a 12-month limit (actually, by now it's been already more than two years). As a result, the single currency depreciated across the board. Against the dollar it fell to 1.2750, i.e. to those very lows which we mentioned yesterday. On their way down the bears may target already at the November lows, which are a figure lower (i.e. at 1.2650). It's quite possible that these levels will be reached, though not necessarily today. The thing is that Eurozone became more homogenized, though in the bad sense of the world. The periphery feels a bit better than before, and the locomotive of the northern countries is moving forward at a lower speed. On Monday it was confirmed by the decrease in Germany's trade surplus and yesterday it could be observed during the bond auction in the country and also when ESM was selling its bills. The protective status of these bonds has faded: yields are growing even in the inflation-indexed bonds. It is good for the European Union in general, but bad for Germany. As to the USA, here the release of fomc's meeting minutes tonight may become the news of the day. No sensations are expected as after that meeting there was Bernanke's press-conference. Anyway, analysts are waiting for this publication with certain caution, which cannot be said about traders who focus their attention on corporations and their quarterly reports. The US stocks are growing due to the favourable statistics, making the rest of the world follow them.

GBP/USD

The sterling received a jolt on the release of the domestic news yesterday. As it turned out, the industrial sector feels not as good as expected. The official statistics pointed at the 0.8% decline in manufacturing activity against the forecasted growth by 0.5%. It's quite a serious breach. Industrial production didn't show any change in the previous month, though it was expected to grow by 0.3%. As a result, the sterling fell against USD from the intraday high at 1.4980 to 1.48, hitting fresh three-year lows. However, there the pair got some support and is now trading at 1.49.

USD/JPY

There's a new tide of profit-taking in the yen. usdjpy from the weekly highs at 101.30 is again on the verge of getting below 100. This is mainly caused by the general tendency to take profits in USD rather than by the events in Japan itself. The move down may get support only at 99.50.

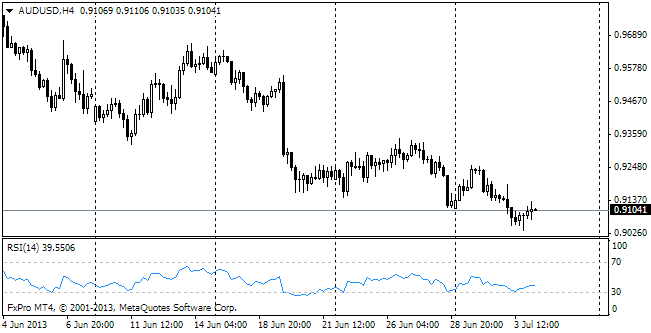

AUD/USD

The aussie is getting modest support. From the beginning of the week the pair has been showing gradual growth. It cannot be called confident yet, but there's no sense in staking against it now. The pair has been overbought in the recent weeks.