EUR/usd

eurusd keeps plying between 1.3490 and 1.3540. Within this narrow range the single currency is expecting important news from Europe, that is the final PMI for the services sector in January and employment in the US private sector by ADP. In the former case analysts on average don't expect any changes, despite the more optimistic estimate for the manufacturing sector a couple of days ago. If the initial estimate is revised up, it may support the single currency as it will shatter doubts about the ECB's tomorrow resoluteness. Yet, stats on the US employment have the greatest risk potential. ADP is expected to announce employment growth by 191K. However, we should remember that a month ago this indicator considerably deviated from the official statistics. Then its growth made 238K, while the BLS stats indicated that employment with civil-service employees excluded increased by 87K. There must be a catch in it: either a considerable revision of ADP statistics to correlate better with the official data (which occasionally happens) or less considerable changes in the last month's estimate by BLS. It's quite possible that it will be both. This month BLS revises models of the seasonal correction and next month ADP may adjust to it. However, this is not all for today. A bit later Non-Manufacturing PMI will be published. It attracts much attention as at the beginning of the week we saw how the similar manufacturing index suddenly dived to the eight-month low. Altogether it makes an interesting lot, though in our opinion the ECB's decision and draghi's commentary to it have a much greater potential to provoke a surge of volatility. We believe that this event is able to confirm a reversal in the euro/dollar or, on the contrary, contribute to appreciation of the pair.

GBP/USD

The British Construction PMI, released yesterday, proved to be the highest since 2007, that is since the time of the housing boom. It would be reasonable to expect a burst of activity after several months of bad weather. It is remarkable that construction was the only sector to show decline in the recent quarter, along with it the PMI remained quite high. A similar deviation was observed earlier, in the previous year, but in construction. Then the economy with a certain delay turned to the path made by estimates of purchasing managers. And it is all because this indicator comprises not only assessment of actual activity, but also orders and price movement. Today there will be a release of Services PMI. The services sector constitutes the overwhelming share of the country's GDP (a bit more than 70%), so divergence from the forecast (59.1 against 58.8 in December) may have a considerable effect on the British currency.

USD/JPY

Yesterday the stock market tried to pull back from the four-month lows and usdjpy also took an attempt to imitate it. The former failed: now S&P futures are at the levels at which they started Tuesday. The pair feels much better now, staying close to 101.30, while yesterday it went as low as 100.70. Despite the scale of the decline the losses of the US and Japanese stock indices still keep within the limits of a correction in the uptrend, though are close to break it.

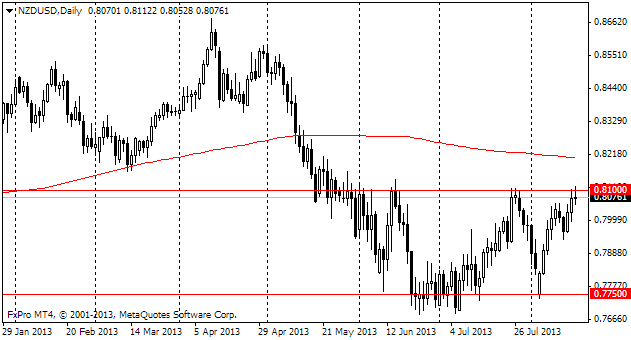

NZD/USD

New Zealand pleasantly surprised with its employment statistics last night. It is growing more evenly than, for instance, in the USA or Great Britain. Here we see that unemployment shrank from 6.2% to 6.0% (as expected) in the fourth quarter, the participation rate increased from 68.6 to 68.9% (better than expected) and the annual rate of salary growth grew from 2.6% to 2.9%. So, it will be quite reasonable if the RBNZ will toughen its policy in March. Yet at this time it will be important to consider how much the Bank is displeased with the high exchange rate and how it is going to fight with it.