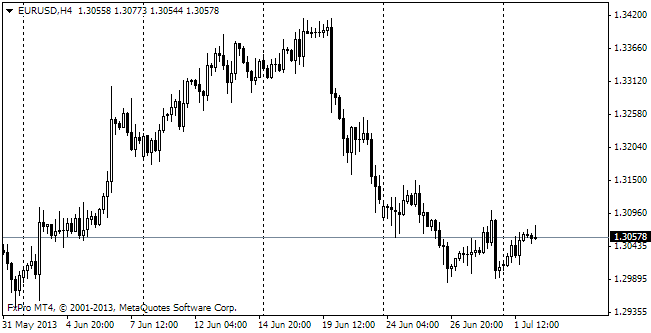

EUR/usd

And though closing of several ministries in the USA didn't provoke any sharp movement, it still put some psychological impact on the dollar. It had sagged by the beginning of the EU session yesterday, which for a while brought eurusd closer to 1.3600. It is amazing that for all that stock markets should feel quite good. For the most part of the day they were in the uptrend. As a result, S&P 500 closed the gap, with which it had started the week, and for a while even returned to the levels of the second half of the previous week. It looks as if it were a common thing! Eventually this confidence spread to the currency markets, where USD again was prone to economic news. Thus, ISM Manufacturing grew to 56.2 in September in comparison with 55.7 a month before and against the expected decline to 55.2. The fact that the employment component of the index keeps growing looks very inspiring for bulls on the threshold of the employment report. The index rose to 55.4 (which is well in the zone of growth), enabling to hope for employment growth in real sectors, which lag much behind the rest in this recovery. As opposed to it, yesterday's data on employment in Germany proved to be much weaker than forecasted. As reported by Federal Labour Agency, unemployment increased by 25K, which was clearly against the market expectations of a 5K decrease. Yet, unlike Germany where September stats were already released, the eurozone got the data only for August yesterday. They showed stabilization of unemployment at the rate of 12.0%, though in big countries like Germany and Italy we again see growth. If the market doesn't sell the euro on such news, it is only because it has turned all its attention to the affairs in the USA. Since there is no hope that the US politicians will come to an agreement in the coming days, the major volatility risks are carried by ADP's labour market report, scheduled for today. It is expected that the index will grow by 177K, approximately like a month ago. It is good enough in comparison with Europe, but is too bad not to think about the stimulus rollback in the near future.

GBP/USD

The British statistics failed to maintain the high recovery pace, which it itself had set earlier, for long. Yesterday's manufacturing PMI proved to be at 56.7 against the previous rate of 57.1. It is surprising that the consensus forecast supposed growth to 57.5. Probably, slacking in growth of the British indicators will become one more signal of the close end of the pound's rally. Today we'll get data on the activity in the construction sector, which is also expected to hit new peaks. The disappointment can throw the sterling off the current 1.6170. Over less than a day the pair has already lost about a figure (the high was at 1.6259).

USD/JPY

The pair is purchased below 97.80, though there are still lots of sellers, who don't let the dollar grow against the yen. Trading in the yen seems to be nervous and deprived of any idea. It is neither flat nor trend. The same situation is observed in other pairs with the yen. So, it would be reasonable to stay away from the Japanese currency now. The stats also point out clear efforts of the BOJ to build up the monetary base, the annual growth rate increased in September already to 46.1%. The target is 100% y/y by April.

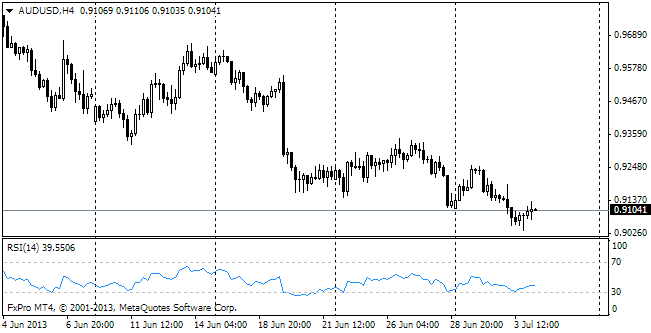

AUD/USD

There's an unpleasant surprise from the Australian statistics. The trade balance in August closed with the surplus of 820bln against the expected 450bln. The expectations that growth of China's imports will improve Australian indicators can't be realized now due to the significant growth of imports. Besides, the preceding data were revised much down (having increased the surplus by about 500bln monthly over the last two years). It is bad but not fatal – the Aussie is still in demand among those, who seek to diversify their portfolios.