EUR/usd

The Asian markets are making slight attempts to recoup the losses, while the US exchanges are balancing in indecision. The indices have fallen by 5% from their high, but yet don't rush to pull back, preferring to wait for the US employment statistics first. In regard to eurusd we can see the formation of a modest uptrend. Having opened at 1.3510 on Wednesday, it closed near 1.3530, yet the intraday low and high were above the corresponding rates of the previous day, and those in their turn were higher than Monday's rates. This modest tendency can be attributed to the market's attempt to take profits after the preceding depreciation of the single currency. There's no complete coincidence in days, but in general the euro/dollar and stock exchanges show a similar tendency: they have come off the highs and are consolidating in expectation of statistics. Besides, the most part of the EU statistics is simply ignored. For example, the final PMI in the services sector, released yesterday, proved to be lower than the initial estimate, the Composite Index made 52.9 against 53.2. Traders can be understood, even in this case the current monthly rate is the highest in two years and a half. Then ADP published its employment rate for the private sector in January. According to these data, the labour market created 175K of new jobs against the expected 191K. The preceding rates were slightly revised down from 238K to 227K. It's quite possible that the agency is waiting for an update of seasonal adjustment models by BLS to carry out a large-scale data revision next month. But it takes time and now we have that neither the relatively good employment data from the USA nor the EU statistics are able to make the euro/dollar change its disposition in expectation of draghi's comments. Altogether we have the US rates, which are not that good, and the EU rates, which are not that bad, as supposed a month ago. It may damp down Draghi's resoluteness to put pressure on the euro and the market resoluteness to get rid of the single currency.

GBP/USD

The British services sector has been slowing down for three months in a row, which can be said by yesterday's PMI. It's worth mentioning that the index is now quite high at 58.3, thus exceeding the average historic rates. Today we will learn the MPC's rate decision. It should be taken into consideration, but there will hardly be any surprises. Most likely, the policy won't be changed and an additional commentary won't be published. It will be much more interesting to watch how the tone of the BOE's comments will change after the release of the quarterly inflation report on February 12. The Bank can use it to convince the markets that policy toughening is not far off.

USD/JPY

The pair has stabilized close to 101.40 following the stabilization in stock indices. Partly the lull in Asia was provoked by the closure of the Chinese market for celebration of the Lunar New Year. Abe has shifted the political focus from the yen to other reforms, in particular those regarding taxation, and is also trying to change the national defense policy. It's hardly about defense of China. There is a feeling that these are attempts to create new sectors in the country.

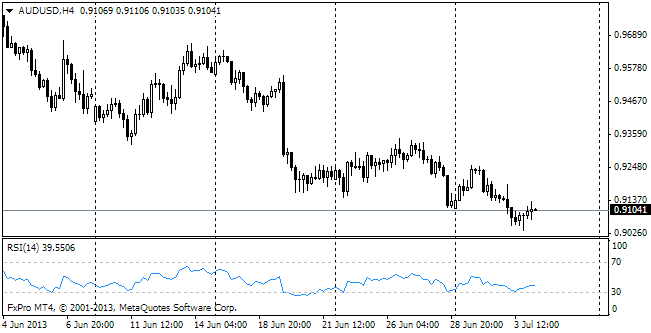

AUD/USD

Last week we wrote that the aussie was tired of falling, but that to start growing it needed positive statistics. And today we've received a small portion of them. Unexpectedly, the country's trade deficit in December came out at 468bln instead of the forecasted 200bln. Retail sales grew by 0.5% that month. The average monthly growth since August totaled the considerable 0.6%. Against last December the sales increased by 5.7%, the highest rate since late 2009.