EUR/usd

The US Federal Open Market Committee tried to avoid in its comments clear hints at the time when tapering would start. Yet, absence of evident concerns regarding the economy let bears gain the upper hand. Stock markets received a severe blow, which is now echoing in the Asian and European markets. S&P 500 shifted away from the global highs, losing more than a percent. Straight after the release eurusd dropped by 85 pips, below 1.37, where it remains now by the beginning of the EU session. The Fed again expressed its desire to see stronger signs of economic growth before withdrawing their support. The message that the housing market has been growing slower this autumn seems to be very important, in our opinion. As you remember, in summer strength of this market made analysts expect the beginning of tapering in September. Now this factor is losing its significance. The housing market appears to live its own life. The summer improvements there didn't contribute to retail sales growth, as we learnt two days ago. Yesterday it also became known that consumer inflation slowed down in September to the annual rate of 1.2%. The Core CPI also showed some slackening, having grown to 1.7% against the expected 1.8%. The Fed also marked decrease in the price growth rate, but added that in the mid-term it is expected to get normal again. The normal inflation rate, as seen by the CB, is 2%. So, now there isn't any significant inflation pressure, which would urge the CB to take action. The most important indicator of the recent years is employment. The partial government shutdown at the beginning of the month postponed the release, so October stats will be published on November 8 instead of tomorrow, as was planned before. Anyway, ADP's private report on employment in the private sector was released on time. It says that in October companies have created 130K of jobs against the expected 150K. Judging by the indicators, the pace of job creation has been slowing down. In June it was 190, in July already 161, in August new jobs grew by 151 and in September by 145. For America such rates are below-trend. Yet employment is not the only thing that should be considered by the Fed. Due to austerity measures and increase in tax receipts the budget deficit is shrinking significantly. This, in its turn, enables Treasury to reduce borrowing. As a result, the amount of idle dollars in the market is growing, which is not very favourable for the dollar in the mid-term. So, don't expect eternal QE.

GBP/USD

The sterling is still in the downtrend and yesterday managed to go below 1.6000 for a while. Now the pair is at 1.6020, but it doesn't cancel the double top, which (if confirmed) will mark a possibility of decline below the current levels.

USD/JPY

The pair is making its way up, despite the correction in the stock markets. Now trading is held at 98.50 and bulls feel like testing the resistance at 99.00. After another meeting the BOJ has decided to keep the policy unchanged, inspired by the growing number of signs of economic improvement.

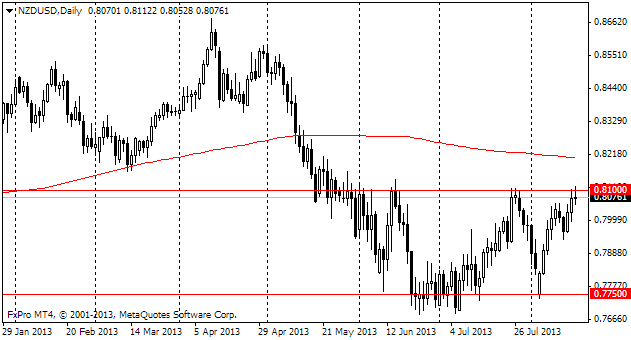

NZD/USD

The New Zealand dollar feels a bit better than others today as the RBNZ pointed out in the commentary to its meeting that growth of the currency may postpone possible increases in the interest rate, putting pressure on inflation. As you remember, for the last two months the Kiwi has appreciated by 11%. In the recent week and a half it has felt slightly worse and lost 3 figures, but still remains above its 200-day MA, which it crossed in mid September.