EUR/usd

The plenty of speeches made by the EU officials yesterday were to the benefit of the single currency. The euro/dollar started growing after Ewald Nowotny had said that the ECB was also seriously considering consequences of different ways to ease the monetary policy, but didn't hurry to apply them. Yves Mersch also pointed out in his speech that the economic recovery in the EU was reducing deflation risks. Actually he said exactly the same thing as we had done before the ECB's meeting last week (‘Don't wait for draghi to be mild'). We were mistaken only about the tone of the governor's comments. He promised (as believed by many) further incentives, but yesterday's comments made it clear that the general approach of the ECB remained the same – the policy will be eased only in case of the economic decline. And the beginning of growth almost automatically removes it from the agenda. Bulls immediately took advantage of difficulties to sell the pair after the rally of USD and brought the euro to 1.3745. From the technical viewpoint we are still within the newly-formed downtrend, while the pair is below 1.3750 till the middle of this week. Breaking above this level or even closing of the week near it will already be a signal to doubt the development of the downtrend in the euro. The German statistics were also in the euro's favour. Though we recommend to pay more attention to data from the periphery, the fact that the annual rate of production growth in Europe's locomotive remained at 5% promises quite favourable industrial production indicators. Over the first two months of this year the index has grown by more than a percent, thus excluding any unpleasant surprises as far as the results of the first quarter are concerned. The Sentix Investor Confidence still shows positive performance. Its fresh April rate makes 14.1. In the entire post-crisis period there were only three months – February-April 2011 – when this index was higher. Investors can be understood. The global economy has significantly increased its growth pace, the periphery bond yields have declined to the record lows or close to them, Ireland has successfully returned to the long-term debt markets and even Greece is planning to do that. Well, no doubts about that. Doubts can be only about the euro's ability to make use of this situation, ignoring the coming toughening of the US monetary policy.

GBP/USD

The cable also made use of the support formed near 1.6560. Despite the decline of the stock market indexes the pair has been trading above 1.6600 since yesterday evening. Technically, it is worth considering the level of 1.6620. It is a former short-term support, which can become a resistance. If it doesn't happen, the chances of another attack on 1.6700 will improve significantly. The main risk for the pound is posed by the release of industrial production data. It is expected that they will show growth by 0.3% for February. The previous week revealed the pair's vulnerability to weakness of statistics.

USD/JPY

The BOJ kept the stimulus programme unchanged, being confident in the continuation of the positive economic performance. Despite the fact that the history questions this confidence, the unexpected surplus of the current account in February made the markets feel more optimistic. The yen, which has been appreciating against most currencies since the end of the last week, is now consolidating at 103.0. Last week's rally has vanished without a trace.

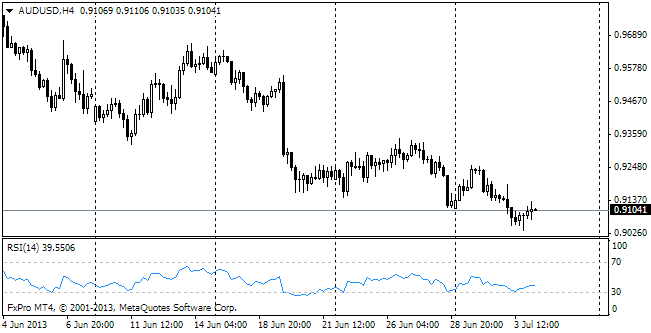

AUD/USD

As soon as the aussie felt more or less confident, business sentiment, on the contrary, began to stagger. The NAB index, published last night, proved to be at the lowest level for the last 8 months. Investors remark decline in sales and ongoing weakness of the labour market. It is an interesting thing – the NAB report forecasts unemployment growth to 6.5% by the end of the year and another rate cut. It is somewhat contradicting to the mood, which the RBA's head expressed when giving comments to the decision on the monetary policy.