EUR/usd

We have a new record of S&P 500 and a new tide of pressure on the single currency. The pair is obviously prevented from going above 1.3800. It was being pushed away from this level since the very beginning of the EU session and after the release of the Final GDP data the euro selling became even more methodical. The final rates proved to be worse than the initial estimates, showing the growth of 0.2% in the fourth quarter of the previous year and the annual rate of 0.4% against the initial 0.3%. France and Germany published their final estimates already last week and they, on the contrary, promised an increase in the general rate. It didn't happen because of weakness of the periphery. It's not the first time that we see how the expensive euro prevents the peripheral economies from getting back to normal. They are quickly losing their growth momentum. It should be taken into account in the ECB, but it is hardly so as the core economies have greater influence on the Bank's policy. So, we shouldn't expect that today draghi will point out that he is more ready to ease the policy than a month ago. The business sentiment indicators still show quite favourable rates, and the economy in general is doing well, so there is no reason to expect that inflation slowdown may become a trigger for easing. Especially when the rate cut will inevitably make them negative, which is terra incognita for the CBs. Europe is the main newsmaker today and yesterday ADP announced its estimation of the US labour market. It is reported that in March employment in the private sector grew by 191K, which is slightly worse than expected (195-200), but the situation was saved by the considerable revision of the February data. Instead of the reported rate of 139K, now the growth for this month is estimated at 178K. The ADP's estimate differed much from the official statistics in the first two months of this year, but now it has been adjusted to correlate better with the BLS data, so we think that Friday's release will contain the rate much similar to what we saw yesterday. In our opinion, even coincidence of the forecasted and actual data may contribute to strengthening of the US dollar, driving the euro/dollar down from the traded area between 1.3750 and 1.3840, which have already bored many.

GBP/USD

The pound remains indifferent to the problems of the euro. Despite depreciation of the latter, gbpusd is in demand and for the last few hours has been trying to get back to 1.6650. Is it a desperate attempt of the bulls to prove their superiority or hope for gathering in the stops above 1.6680? Or is it probably a stake on the possibility that the BOE will start toughening its policy already this year, forestalling the US Fed? It's possible in theory as before the crisis England lived with higher rates than the States, but even then they were not enough to curb the housing boom in the country. And now we get alarming signs of new overheating in this sector. In our opinion, it is too early to raise the rates and the British economy will still have to face slowdown of the current GDP growth and inflation decline.

USD/JPY

Yesterday the pair slowed down its growth and with great difficulty reached 104.0 last night. In short term, bulls may need a break before continuing the rally and progressing to a new level. Anyway, while the market is growing, the pair may follow it. So it only remains to hope that the US employment won't be disappointing.

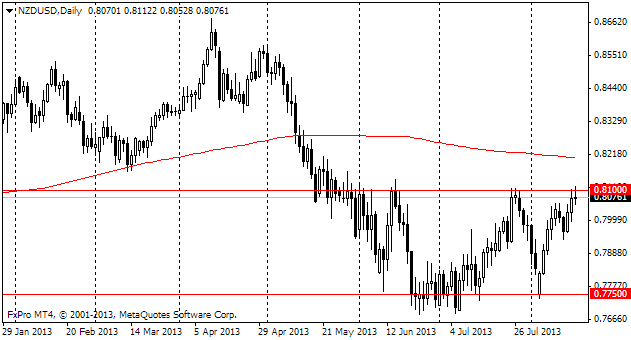

NZD/USD

The Kiwi keeps falling. We supposed that it could perform that way, saying that the pair was not steady above 0.8500. Now trading is held at 0.8550, so the pair has corrected its position already by a figure and a half since the beginning of the week. It's scarcely the end, possibly decline to 0.8440 will happen already before the middle of the coming week.